Mickey Kim

By Mickey Kim

Guest columnist

What if I told you just 10 companies in the S&P 500 now account for nearly 40% of what millions of Americans consider their “diversified” retirement portfolio?

Most people think of the S&P 500 as a proxy for the U.S. stock market or diversified portfolio of America’s largest companies. On the surface, that isn’t wrong—the S&P 500 Index includes 500 large U.S. companies across many industries and captures about 80% of the total U.S. market capitalization.

But here’s the rub: because the S&P 500 is market capitalization-weighted, the biggest companies dominate its performance.

To see how dramatic this concentration has become, at the beginning of 2025 Apple (Nasdaq: AAPL) had a market capitalization of about $3.8 trillion (roughly $250 per share x 15.2 billion shares outstanding), giving it a 7% weighting in the S&P 500—just one company representing nearly one-fourteenth of the entire index.

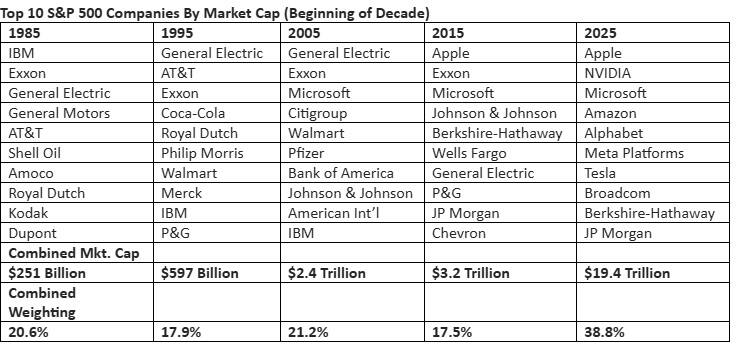

As the table shows, the 10 largest companies (10/500 or just 2% of the index) now make up about 39% of its total weight. That’s more than double their share a decade ago—and their combined market value has increased roughly six-fold. To put today’s scale in perspective, the individual market capitalizations of Apple, NVIDIA and Microsoft each exceeded the combined market capitalization of the ten largest companies just ten years ago.

For millions of Americans, their 401(k) or IRA is their largest financial investment—and many of those accounts are tethered to S&P 500 index funds, either directly or through target date funds. These funds are designed to mechanically buy and sell stocks based solely on their index weights and marketed as cheap, efficient ways to “own the market.” Unfortunately, the S&P 500 increasingly behaves less like a broad market portfolio and more like a mega-capitalization technology fund.

Investors have benefitted enormously over the past three years from the spectacular performance of this small handful of massive technology stocks, much of it fueled by investor enthusiasm for artificial intelligence. But this concentration creates a dangerous asymmetry: investors get all the downside when these giants stumble, but the upside is increasingly limited to fewer companies.

Consider the “Magnificent 7” stocks that dominated S&P 500 performance for several years, but their leadership has significantly narrowed. As Charlie Bilello of Creative Planning noted, from the start of 2025 through Feb. 5, 2026, only Alphabet (74.7%) and NVIDIA (28.0%) outperformed the S&P 500 (17.2%) on a total-return basis. Meta Platforms (14.8%), Apple (10.7%) and Amazon (1.5%) posted positive returns but lagged the index, while Tesla (-1.6%) and Microsoft (-5.9%) posted negative returns.

As The New York Times warned in “Your ‘Safe’ Stock Funds May Be Riskier Than You Think,” “if the biggest trees fall, everyone will feel the forest shake.”

History is littered with fallen giants—IBM, General Electric and others—underscoring the old adage “trees don’t grow to the sky.” As the table illustrates, IBM was “King of the Hill” in 1985, dropped to 10th by 2005 and was out of the Top 10 entirely by 2015. There’s very little “persistence” among market leaders—today’s giants rarely stay giants. Innovation shifts. Business models are “disrupted.” Competition never sleeps.

This raises an important question: does your portfolio strategy truly account for concentration risk?

Diversification isn’t about owning more stocks—it’s about owning different sources of return. Achieving that may require looking beyond traditional market-cap-weighted index funds to obtain the stability many investors assume they already have.

IBJ graphic

IBJ graphic

{kind=link}